Tax Implications of Change in Revenue Recognition for Franchisors

Many franchisors are already aware that, under the FASB ASC 606, their GAAP financial statements now need to implement new revenue recognition standards. Some franchisors may even have an in-depth understanding as to what ASC 606 means to their financial statements. However, do they know how the new standard will affect taxable income over the next few years?

There are several rules that need to be taken into account crossing over from the Internal Revenue Code to the Accounting Standards Codification. With regard to implementation of ASC 606, there are three important notes to understand:

- For GAAP purposes, a portion of revenues may be recognized earlier than in prior years

- For GAAP purposes, a portion of revenues may be recognized much later than in prior years

- For Tax purposes, revenues must be recognized the earlier of when the amounts are recognized on your audited financial statements, or the year following the year of receipt

Below is a simple and realistic scenario to illustrate the different tax results before and after implementation of ASC 606.

Joe’s Jelly Jar, Inc.

A franchisor, Joe’s Jelly Jar, Inc., signs a 10-year franchise agreement on 1/1/18 and receives a $50,000 upfront franchise fee at execution. Joe’s Jelly Jar provides separate and distinct training services during 2018, valued at $10,000, which is included in the upfront franchise fee. The franchisee commences operations during 2019.

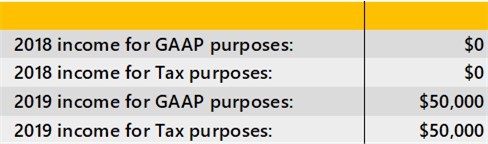

Prior to ASC 606

Joe’s Jelly Jar has no revenues in 2018 for book or tax. Franchise fees for Joe’s Jelly Jar, for GAAP purposes, were generally recognized when the franchisee commenced operations, which, in our case, didn’t occur until 2019. For tax purposes, revenues are recognized the earlier of the year that they are recognized on the audited financial statements, or the succeeding taxable year. Since the $50,000 was deferred on the audited financial statements prior to the franchisee commencing operations, it could be deferred for tax purposes until 2019, at the latest.

Fig 1.

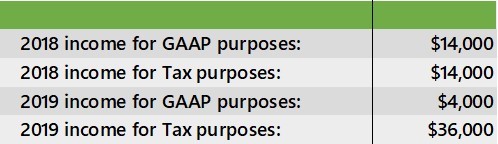

After ASC 606

Franchise fees for GAAP purposes need to be analyzed to identify separate and distinct performance obligations, then the franchise fee would be allocable to those separate and distinct performance obligations, and revenues would be recognized either at a point in time, or over time, as the obligations are settled. In this example, Joe’s Jelly Jar has determined that they provide 2 separate and distinct performance obligations; 1) the licensing of symbolic intellectual property, and 2) the general business training that it provides to the franchisee, prior to the franchisee commencing operation. The allocation of the franchise fee is determined to be $40,000, allocable to the licensing of symbolic intellectual property, and $10,000 allocable to the separate and distinct general training services. The recognition of these revenues would be $4,000 for the licensing of IP (1/10th of the term of use), plus $10,000 for the training services recognized as those services are provided.

For tax purposes, Joe’s Jelly Jar still has to recognize revenues the earlier of the year that they are recognized on the audited financial statements, or the succeeding taxable year. Since Joe’s Jelly Jar recognized the $14,000 in 2018 on the audited financial statements, it would be recognized for tax purposes as well. The remaining $36,000 of the franchise fee would be recognized over the next 9 years for GAAP purposes (term of the franchise agreement), but fully recognizable for tax purposes in 2019 (succeeding taxable year).

Fig 2.

As you can see in Figure 2, after the implementation of ASC 606, Joe’s Jelly Jar is forced to accelerate taxable income recognition of $14,000 in 2018. The “good news” is that, the implementation of ASC 606 is considered a change in method of accounting. When a new method of accounting is adopted, IRC section 481(a) requires an entity to take into account adjustments to income for the taxable year before the change under the old method, as well as, income for the year of change and subsequent years under the new method - as if the new method had always been used. If a 481(a) adjustment is net positive to taxable income, a franchisor can account for the increase to taxable income ratably over a four-year period, beginning in the year of change. So, in our example of $14,000 of accelerated income, the IRC 481(a) adjustment would allow Joe’s Jelly Jar to extend the recognition of additional taxable income of $3,500 each year in 2019, 2020, 2021, and 2022.

This is an over-simplified example, and if a franchisor is selling/opening 10, 50, or 100 units each year, the level of volume and complexity in this analysis is significantly higher. I know the adage, “every situation is different” sounds cliché; but, every situation is different, so please discuss your specific circumstances with your advisor and make sure that the tax consequences of your implementation are properly planned for to prevent any headaches or surprises. If you have any questions regarding this tax implication, or how it may affect you, please contact Bob Gilbert.